Residential Roof Depreciation Life

Roof Insurance Claim Process Questions Bob Behrends Roofing Gutters

Rental Property Depreciation Rules Schedule Recapture

Roof Deductible L Depreciation L Roof Insurance Claim Specialists Bbr Contracting Residential Commercial Roofing Services

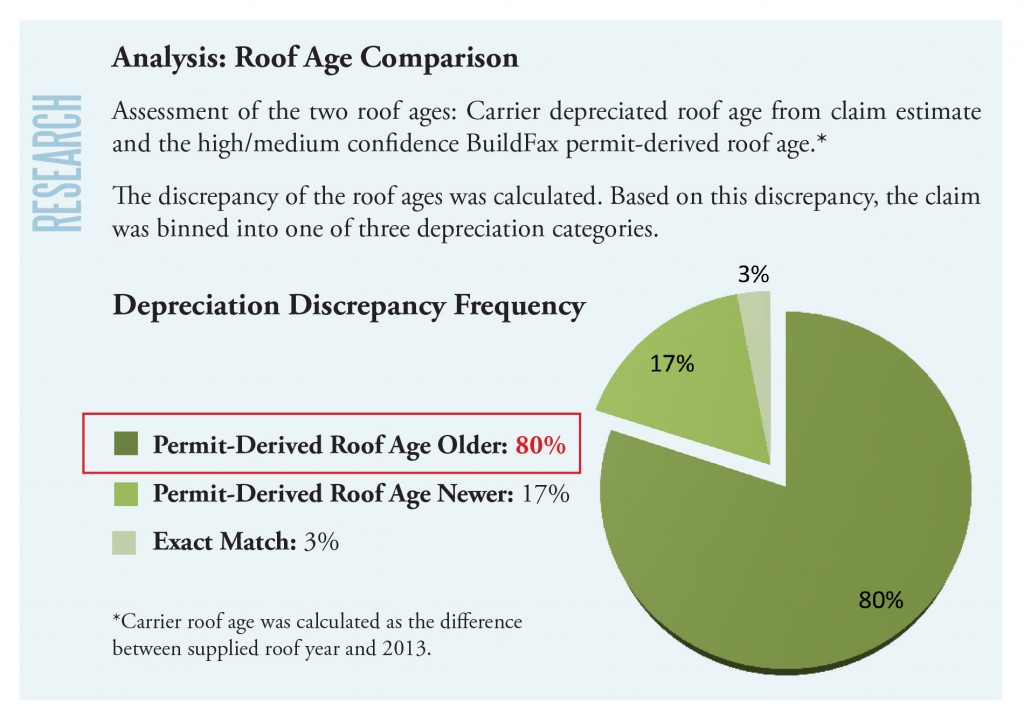

Part Three The Value Of Accurate Roof Age In Claims

How Does Recoverable Depreciation Impact My Home Insurance Claim Valuepenguin

What Is The Depreciation Of The Roof On A Commercial Building

Life expectancy of building components will vary depending on a range of environmental conditions quality of materials quality of installation design use and maintenance.

Residential roof depreciation life.

My Roof Needs To Last How Long

What Is Qualified Leasehold Improvement Property

Depreciation Life On Permanent Houseboat Used As R Intuit Accountants Community

What Is Rental Property Depreciation

Calculating Roof Depreciation In An Insurance Claim The Voss Law Firm P C

The 2020 Ultimate Guide To Irs Schedule E For Real Estate Investors

Can I Make Money Off My Insurance Roofing Claim Slade Roofing

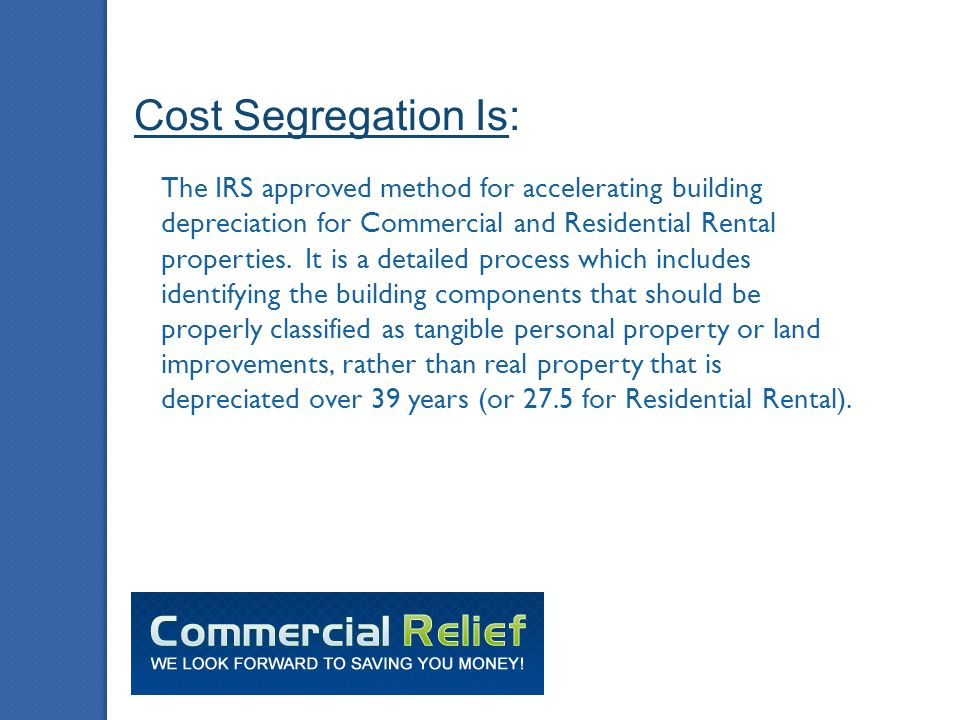

What Is Cost Segregation The Irs Approved Method For Accelerating Building Depreciation For Commercial And Residential Rental Properties It Is A Detailed Ppt Download

How Bonus Depreciation Affects Rental Properties Millionacres

Irs Issues Guidance For Change To Real Property Depreciation Grant Thornton

An Introduction To Solar Depreciation Yellowlite

Cost Segregation Residential Rental Property Cost Segregation Study

Retired Military Finances 201 Understanding Depreciation Recapture C L Sheldon Company

How To Calculate Depreciation On Rental Property

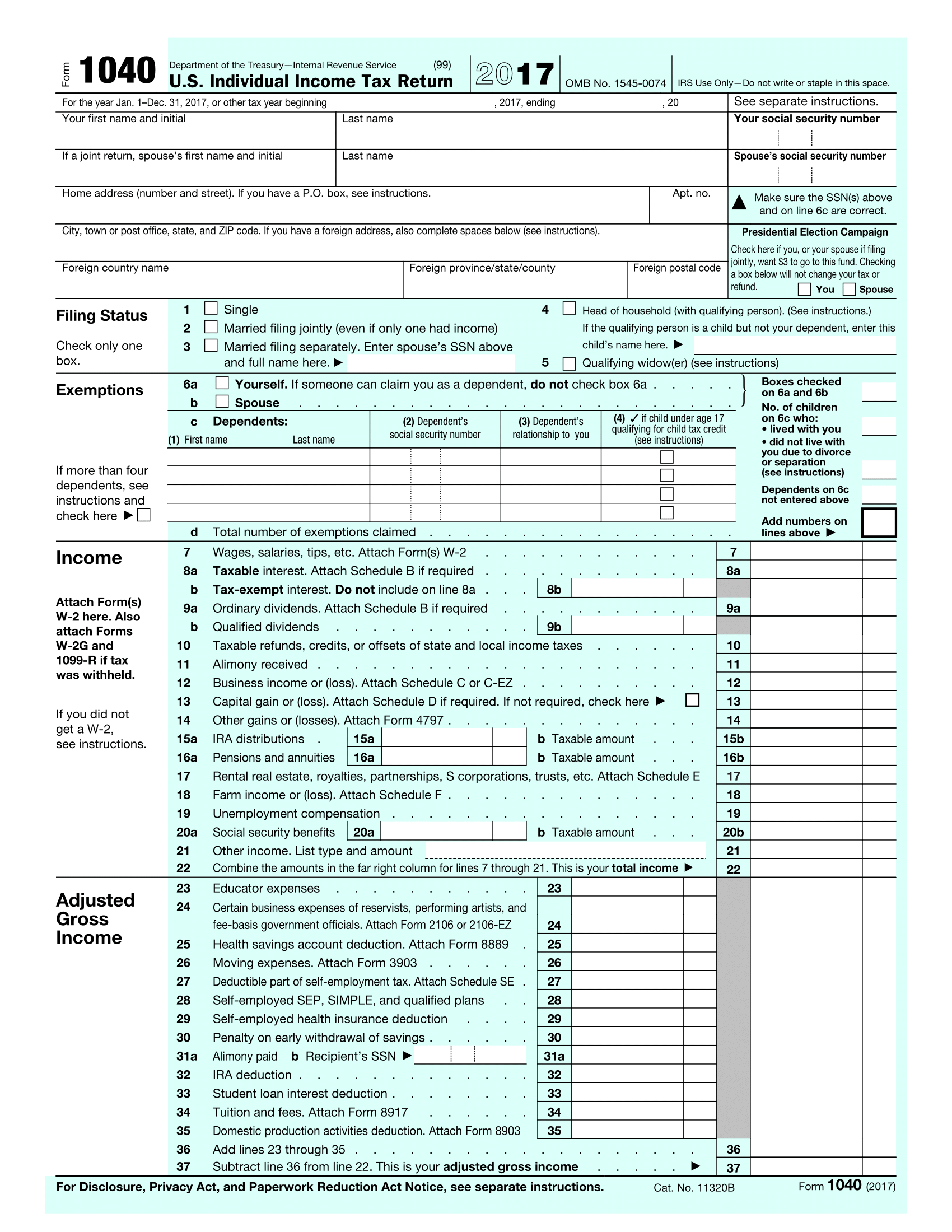

Liberty Tax Service Online Basic Income Tax Course Lesson Ppt Download

Residential Rental Property Depreciation Calculator

Prateek Grand City Bharosa Jyada Prateek Ka Vaada With Images Property Valuation Melbourne City

5 Tax Deductible Home Improvements For 2018 Budget Dumpster

What Is Rental Property Depreciation And How Does It Work

Understanding Depreciation Recapture Taxes On Rental Property Rental Property Being A Landlord Military Housing

Https Tax Thomsonreuters Com Content Dam Ewp M Documents Tax En Pdf Other Quickfinder Updates Qde Supplement Update Pages Pdf

What Residential Roof Warranties Will Cover In Kansas City Pyramid Roofing

4562 Half Year Mid Month And Mid Quarter Conventions 1120 1120s 4562

Section 179 Expensing What You Need To Know For The 2019 Tax Year Cherry Bekaert

23 Items For Depreciation On Your Triple Net Lease Property Net Lease Tax Deductions Capital Gains Tax

How To Depreciate Rental Of A Principal Residence Home Guides Sf Gate

The Dirt On Property Depreciation Property Investment Property Tax Time

Https Nanopdf Com Download Depreciation Appraisal Institute Pdf

2020 Guide To Solar Tax Credit Rebates And Other Incentives

How Does Depreciation Work Millionacres

Roofing Contract Template 145 Roofing Contract Contract Template Roofing

Depreciable Life Life Expectancy For Rental Purchases

Insurance Claims Top That Roofing Denver Co

Housing In Japan Wikipedia

What Is The Lifespan Of A House Swiss Life Group

Suprising Advice That Will Make Your Home Improvement Project Go Smoothly Home Improvement Projects Home Decor Shops Barn House Kits

Tax Benefits On Multi Family Projects Capstan Tax Strategies

Http Www Saepc Org Assets Councils Southernarizona Az Library Oliverhandouts Pdf

Depreciation Strategies Under The New Tax Law What You Need To Know Counselors Of Real Estate

Tax Savings Rental Property Depreciation Explained Fox Business

2019 Year End Tax Letter Tax Reform Full Expensing Of Assets Baker Tilly

Tennessee Insurance Litigation Blog By Brandon Mcwherter Parks T Chastain

Appreciating Vs Depreciating Assets The Free Financial Advisor

Solar Tax Credits And Benefits Part 2 Of Our Commercial Solar Installation

Source : pinterest.com